Please wait as we load hundreds of rigorously documented facts for you.

Please wait as we load hundreds of rigorously documented facts for you.

For example:

In accord with the standard practice of economists and government agencies, many of the debt, spending, and revenue figures in this research are expressed as a portion of annual U.S. economic output, or gross domestic product (GDP). This is because debates about the size of government and the effects of its debt are frequently centered upon how much of a nation’s economy is consumed by government. This measure also accounts for population growth, moderate inflation, and the relative capacity of governments to service their debts.[1] [2] [3] [4] [5] [6] [7] [8]

However, the federal government cannot appropriate the entire U.S. economy to pay its debts. This is because private citizens—who produce the goods and services that comprise the bulk of the economy—use most of these resources to live. Also, state and local governments consume some of the nation’s GDP. Hence, this research sometimes expresses federal debt as a portion of annual federal revenues. This is a more direct measure of the federal government’s capacity to service its debts.

In keeping with Just Facts’ Standards of Credibility, all charts in this research show the full range of available data, and all facts are cited based upon availability and relevance, not to slant results by singling out specific years that are different from others.

* As of April 1, 2024, the U.S. Treasury’s official figure for the debt of the federal government is $34.6 trillion, or more precisely, $34,627,201,333,064.[9] This equates to:

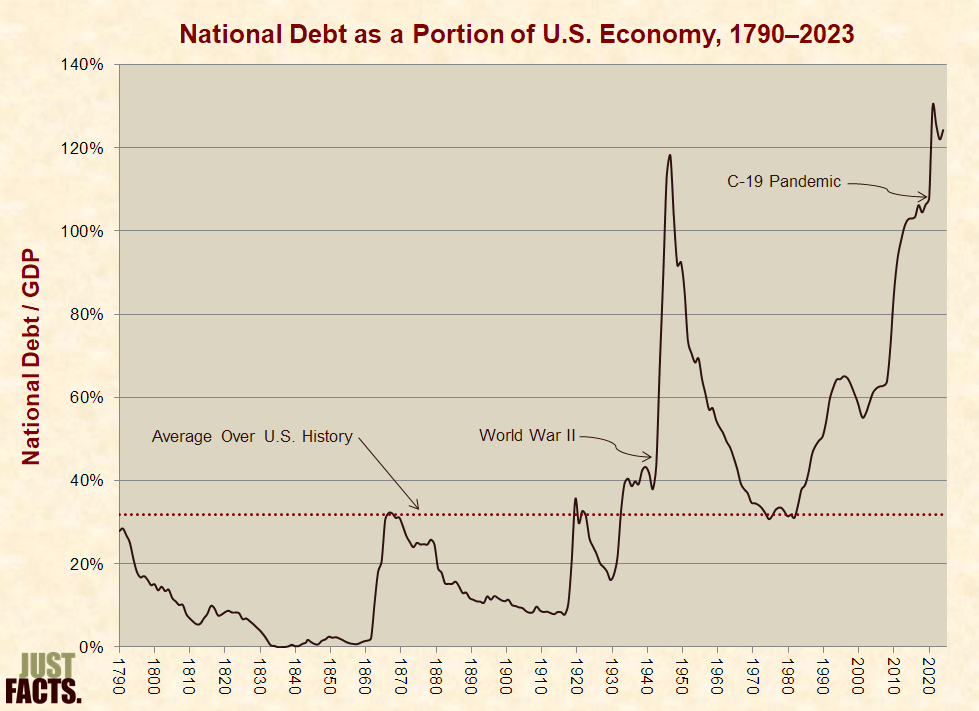

* During 2022, while the national debt was 123% to 127% of GDP,[15] [16] some organizations and individuals claimed it was 98% to 100%.[17] [18] [19] These lower figures don’t account for the full national debt but omit a portion of it called “debt held by government accounts.”[20] [21] [22] [23] For more facts about this issue, see the section below on government accounting.

* Over the course of U.S. history, the national debt has averaged 32% of the nation’s GDP.[24]

* In May 2020 (two months after the outset of the Covid-19 pandemic[25]), the national debt reached 120% of GDP, breaking a record set in 1946 for the highest level in the history of the United States. The previous record of 118% stemmed from World War II, the deadliest and most widespread conflict in world history.[26] [27]

* At the end of 2023, the national debt was 124% of GDP, or 3.9 times its average over U.S. history:

* For additional facts and a video about the magnitude, causes, and consequences of the surge in government debt over recent decades, visit Just Facts’ article “National Debt Breaks All-Time Record for Highest Portion of U.S. Economy.”

* Per the U.S. Government Accountability Office, which is the official watchdog of Congress:[29]

* Federal law requires publicly traded corporations to account for their “explicit” and “implicit” liabilities and obligations. These include employee pensions and other financial burdens that companies have accrued but not paid for yet. This type of bookkeeping is called “accrual accounting.”[32] [33] [34] [35]

* At the close of its 2022 fiscal year, the federal government had accrued roughly:

* The figures above are determined with federal data in a manner that approximates how publicly traded corporations are required by law to report their liabilities and obligations.[42] [43] [44] [45] [46] The unfunded obligations of Social Security and Medicare reflect how much money must be immediately placed in interest-bearing investments to cover the projected shortfalls for all of the programs’ current participants (both taxpayers and beneficiaries). These shortfalls are equal to:

* Balanced against the value of its commercial assets,[50] the federal government had a combined total of $135.5 trillion ($135,487,000,000,000) in debts, liabilities, and unfunded obligations at the close of its 2022 fiscal year.[51] This shortfall equates to:

* The figures above don’t account for the unfunded obligations of any federal policies or programs other than Social Security and Medicare.[58] [59]

* The unfunded obligations of Social Security and Medicare are based on current federal laws, federal data, and federal economic and demographic projections.[60] [61] [62] With regard to these factors:

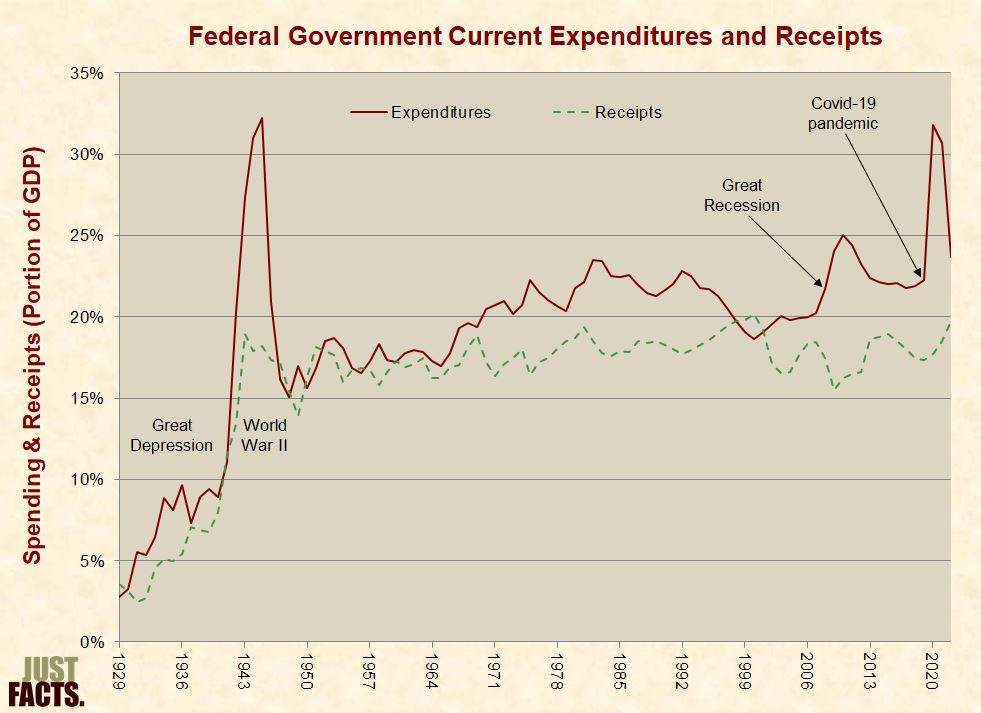

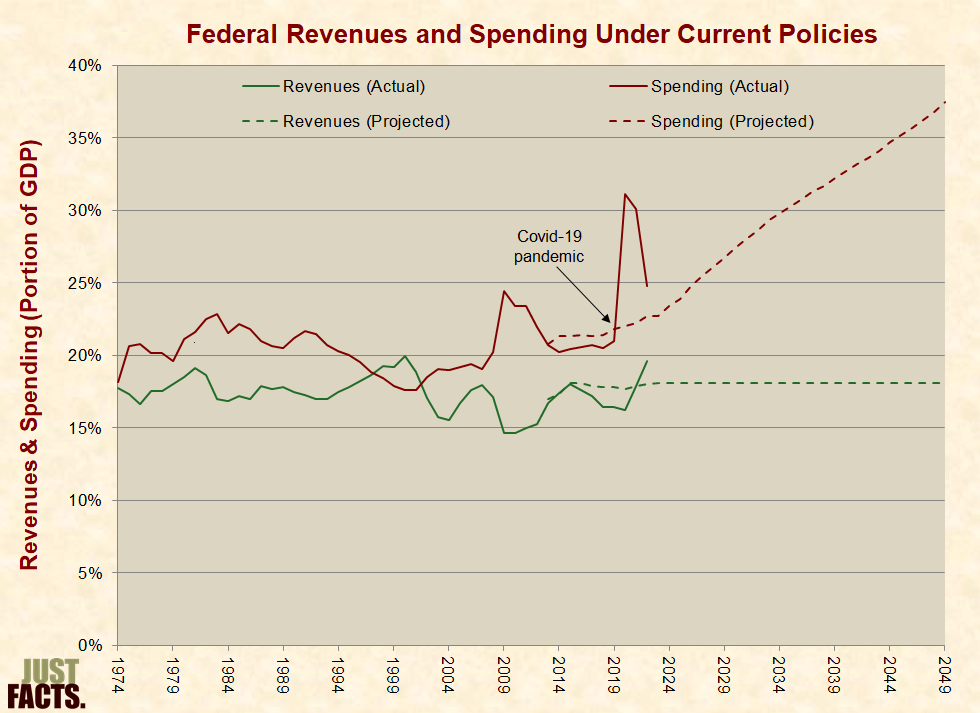

* From 1929 to 2022, federal government current expenditures and receipts—as a portion of gross domestic product—have varied as follows:

* Data from the chart above:

|

Year |

Receipts |

Expenditures |

|

1930 |

3% |

3% |

|

1940 |

8% |

9% |

|

1950 |

16% |

16% |

|

1960 |

17% |

17% |

|

1970 |

17% |

20% |

|

1980 |

19% |

22% |

|

1990 |

18% |

22% |

|

2000 |

20% |

19% |

|

2010 |

16% |

25% |

|

2020 |

18% |

33% |

|

2022 |

20% |

24% |

* From 1959 to 2022, the portion of federal government outlays that were spent on:

* Data from the chart above:

|

Category |

Portion of Federal Current Spending |

|||||||

|

1960 |

1970 |

1980 |

1990 |

2000 |

2010 |

2020 |

2022 |

|

|

Social Programs |

21% |

32% |

44% |

44% |

54% |

61% |

73% |

64% |

|

National Defense & Veterans’ Benefits |

53% |

42% |

27% |

25% |

19% |

20% |

14% |

17% |

|

General Government & Debt Service |

19% |

18% |

21% |

25% |

20% |

13% |

10% |

15% |

|

Economic Affairs |

6% |

7% |

7% |

5% |

5% |

4% |

3% |

4% |

|

Public Order & Safety |

0% |

0% |

1% |

1% |

1% |

2% |

1% |

1% |

* A scientific, nationally representative survey commissioned in 2020 by Just Facts found that 50% of voters believe social spending is not the main cause of rising national debt.[72] [73] [74]

* From 1979 to 2020, the effective federal tax rates paid by households of different incomes have varied as follows:

* Data from the chart above for 2019, prior to the Covid-19 pandemic:[78]

|

Average Effective Federal Tax Burdens (2019) |

|||

|

Income Group |

Income |

Tax Rate |

Taxes Paid |

|

Lowest 20% |

$39,100 |

0.3% |

$100 |

|

Second 20% |

$59,600 |

7.7% |

$4,600 |

|

Middle 20% |

$85,500 |

12.4% |

$10,600 |

|

Fourth 20% |

$124,900 |

16.5% |

$20,600 |

|

Highest 20% |

$333,100 |

24.3% |

$81,100 |

* Breakdown of the highest 20%:

|

Income Group |

Income |

Tax Rate |

Taxes Paid |

|

81st–90th |

$181,300 |

19.9% |

$36,000 |

|

91st–95th |

$250,400 |

22.0% |

$55,000 |

|

96th–99th |

$417,400 |

24.4% |

$101,800 |

|

Top 1% |

$1,998,700 |

30.0% |

$600,300 |

* Data from the chart above for 2020—amid Covid-19 government lockdowns and intensified social spending:[79] [80] [81]

|

Average Effective Federal Tax Burdens (2020) |

|||

|

Income Group |

Income |

Tax Rate |

Taxes Paid |

|

Lowest 20% |

$42,200 |

–8.8% |

–$3,700 |

|

Second 20% |

$63,600 |

0.6% |

$400 |

|

Middle 20% |

$90,500 |

7.0% |

$6,300 |

|

Fourth 20% |

$131,800 |

12.7% |

$16,800 |

|

Highest 20% |

$360,900 |

23.6% |

$85,200 |

* Breakdown of the highest 20%:

|

Income Group |

Income |

Tax Rate |

Taxes Paid |

|

81st–90th |

$191,500 |

17.6% |

$33,700 |

|

91st–95th |

$265,100 |

21.1% |

$55,900 |

|

96th–99th |

$440,000 |

24.1% |

$106,200 |

|

Top 1% |

$2,291,800 |

29.9% |

$686,300 |

* A scientific, nationally representative survey commissioned in 2019 by Just Facts found that 79% of voters believe middle-income households pay a greater portion of their income in federal taxes than the top 1%.[82] [83] [84]

* Per the U.S. Government Accountability Office, when the federal government spends more than it collects in revenues, the resulting debt is “borne by tomorrow’s workers and taxpayers.”[85]

* As detailed in publications of the Government Accountability Office, the Congressional Budget Office, the Brookings Institution, and Princeton University Press, excessive government debt can cause:

* Because association does not prove causation, and because numerous factors can affect economic outcomes, there is frequently no objective way to isolate the effects of a single factor (like government debt) on a single outcome (like wages or inflation).[101] [102] [103] [104]

* The consequences of government debt can manifest slowly over the course of decades or suddenly in a few years or less.[105] [106] [107]

* The most accurate measure of nations’ living standards is their household consumption of goods and services.[108] [109] This is “preferred welfare indicator” of the World Bank.[110] [111]

* Some people claim that nations with their own currencies suffer minimal consequences from high national debts. They say this is because these nations can always print more money to finance their debts. People who make this argument commonly compare the high-debt nations of Japan and Greece while alleging that Japan (which has its own currency) has not economically suffered like Greece (which does not have its own currency).[112] [113] [114] [115] [116]

* As Japan’s national debt surged in the 1990s and 2000s,[117] the nation had much slower growth in its living standards than Greece. Near the end of this period, Greece’s government debt bubble burst, and it experienced a sudden collapse in living standards.[118] Ultimately, the debt-burdened nations of Japan and Greece ended up in about the same place:

* Gross domestic product (GDP) is the standard measure of nations’ economic output. It is equal to the value of all goods and services that a country produces in a year minus the resources used to produce them.[120] [121]

* GDP divided by population is often used to measure a country’s standard of living. Per the textbook Macroeconomics for Today:

* In 2012, the Journal of Economic Perspectives published a study about the economic consequences of government debt based on 2,000+ data points on debt and economic growth across two centuries and 20 advanced economies (like the United States, France, and Japan). The authors of this paper, Carmen M. Reinhart of the University of Maryland, Vincent R. Reinhart of Morgan Stanley, and Kenneth S. Rogoff of Harvard University:

* In April of 2013, the Political Economy Research Institute at the University of Massachusetts, Amherst, published a working paper that was widely cited by media outlets as evidence that large national debts don’t harm economies.[128] [129] The authors of this paper, Thomas Herndon, Michael Ash, and Robert Pollin:

* In 2022, the interest on the national debt was $775 billion, or more precisely, $774,679,343,619.[139] This amounts to:

* In federal fiscal years 1962 to 2022, interest on the national debt ranged from 9% to 27% of federal revenues, with a median of 16% and an average of 17%. In 2022, the interest on the national debt was 15% of federal revenues:

* The primary factors that affect interest costs are the amount of debt owed and the interest rates charged on that debt.[148] [149] [150]

* Even though the national debt is currently a larger portion of the U.S. economy than any era of the nation’s history, interest on the debt is currently about the same as historical norms. This is because the average interest rate on the debt has been much lower than in the past. However, the Congressional Budget Office “anticipates” that interest “payments will increase considerably as interest rates return to more typical levels.”[151] [152]

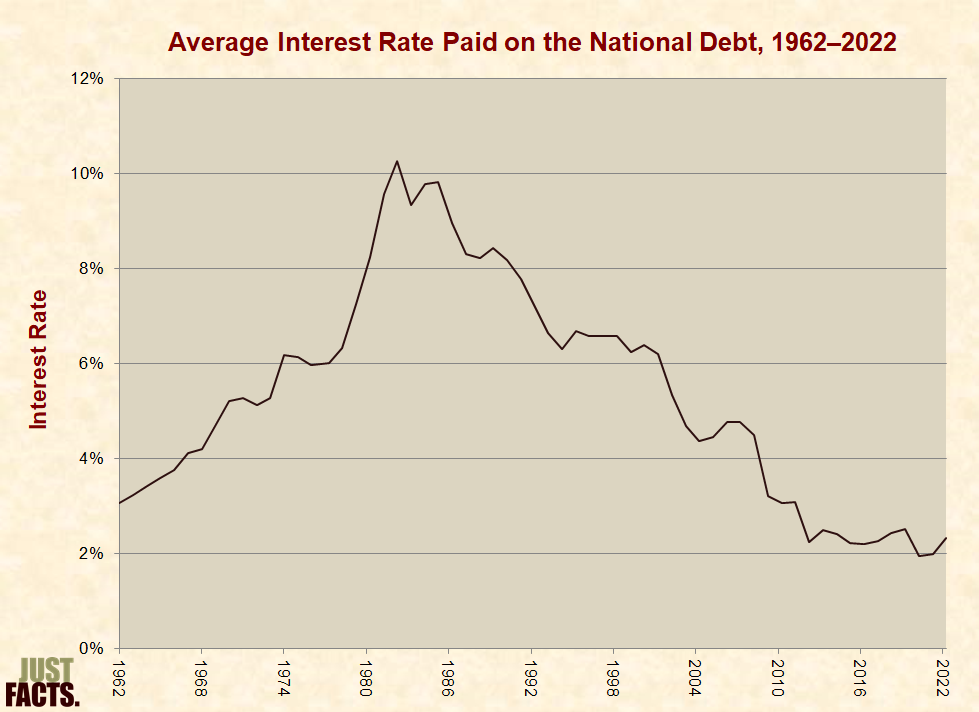

* In federal fiscal years 1962 to 2022, the average annual interest rate on the national debt ranged from 1.9% to 10.3%, with a median of 5.3% and an average of 5.4%. In 2022, the rate was 2.3%:

* In 2022, the average interest rate on debt held by the public was 2.2%, and the average interest rate on intergovernmental debt was 3.4%.[154]

* Per the Congressional Research Service, the Federal Reserve, the Congressional Budget Office, and the White House Office of Management and Budget, the following factors affect interest rates on the debt held by the public:

* When deciding the term length (maturity) of the debt it issues, the Treasury tries to balance the benefit of lower costs from short-term interest rates with the benefit of having predictable payments on long-term debt.[180] At the end of 2022, the average maturity of outstanding debt was 74 months—approximately 14 months longer than the historical average of 60 months.[181] [182]

* Interest rates on intergovernmental debt are affected by the same drivers as debt held by the public.[183] [184]

* The interest rates on most intergovernmental debt are based on the average interest rate of long-term debt held by the public. This applies regardless of whether the intergovernmental debt is short-term or long-term.[185] [186] [187] [188] [189] [190]

* Since long-term debts generally have higher interest rates than short-term debts, interest rates on intergovernmental debt tend to be higher than interest rates on debt held by the public.[191] [192] [193] [194] In 2022, the average interest rate on debt held by the public was 2.2%, and the average interest rate on intergovernmental debt was 3.4%.[195]

* The Social Security Trust Fund—which makes up roughly 41% of all intergovernmental debt—starts all new investments as short-term debt scheduled to mature on the upcoming June 30th. On June 30th, the matured debt and its interest are rolled into new debts of different maturities ranging from 1 to 15 years.[196] [197] [198]

* Regardless of the maturity of a debt, federal trust funds can demand repayment with interest at any time if they need the money to cover their expenses. This feature makes these investments similar to cash from a liquidity perspective.[199] [200] [201]

* The U.S. Constitution vests Congress with the powers to tax, spend, and pay the debts of the federal government. Legislation to carry out these functions must be enacted in one of the following ways:

* Other factors impacting the national debt include but are not limited to inflation, legislation passed by previous Congresses and presidents,[203] economic cycles, terrorist attacks, pandemics, natural disasters, demographics, and the actions of U.S. citizens and foreign governments.[204] [205] [206]

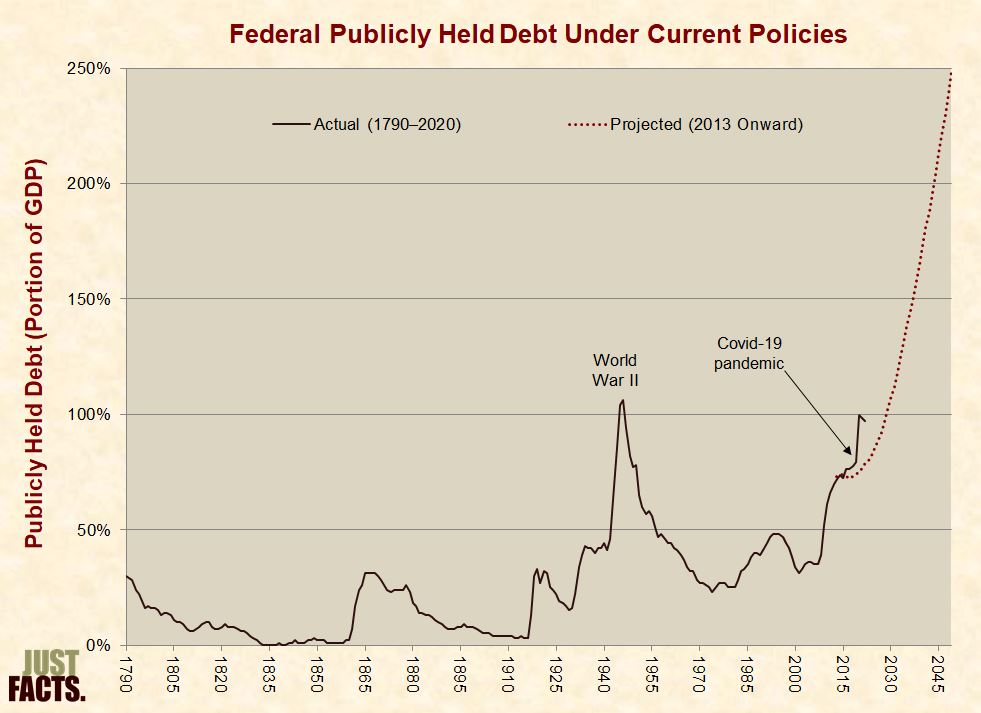

* In 2013, the Congressional Budget Office projected the publicly held debt that the U.S. government would accumulate under current federal policies and their economic effects.[207] [208] Combining these projections with historical data and actual outcomes since then yields the following results:

* Other than interest on the national debt, most of the long-term projected growth in federal spending is from Medicare, Medicaid, Social Security, the Children’s Health Insurance Program, and the Affordable Care Act (a.k.a. Obamacare).[214] [215]

* Per the Congressional Budget Office, postponing action to stabilize the debt will:

* World War II began in 1939, the U.S. joined it in 1941, and it ended in 1945.[219] It was the deadliest and most widespread conflict in world history, claiming 40–50 million lives.[220] In 1946, the U.S. national debt reached 118.4% of the U.S. economy (GDP), the highest it had ever been in the history of the United States until this record was broken in May of 2020.[221]

* The following Ph.D. economists and political scientists have claimed that high levels of national debt during World War II prove that the modern national debt is not a serious threat:

* None of the publications above mentioned that in the 40 years that followed the end of World War II (1946–1985):

* In 2010, around the time when the scholars made the claims above, the Congressional Budget Office projected that under current policies and a sustained economic recovery over the next 40 years:

* By the end of 2022, the total national debt had risen to 123% of GDP, or 4% above the peak of World War II.[233]

* As alternatives to the current policy projections above, the Congressional Budget Office has also run projections for scenarios such as these:

1) Current law:[234]

2) Republican Congressman Paul Ryan’s 2014 budget resolution, called the “The Path to Prosperity”:[242]

* Combining historical data on the national debt with the Congressional Budget Office’s 2014 projections for current policy, current law, and the Ryan plan yields the following results:

* Other than interest on the national debt, most of the long-term projected growth in federal spending under the Congressional Budget Office’s current policy and current law scenarios stems from Social Security, Medicare, Medicaid, the Children’s Health Insurance Program, and Affordable Care Act (a.k.a. Obamacare) subsidies.[258] [259]

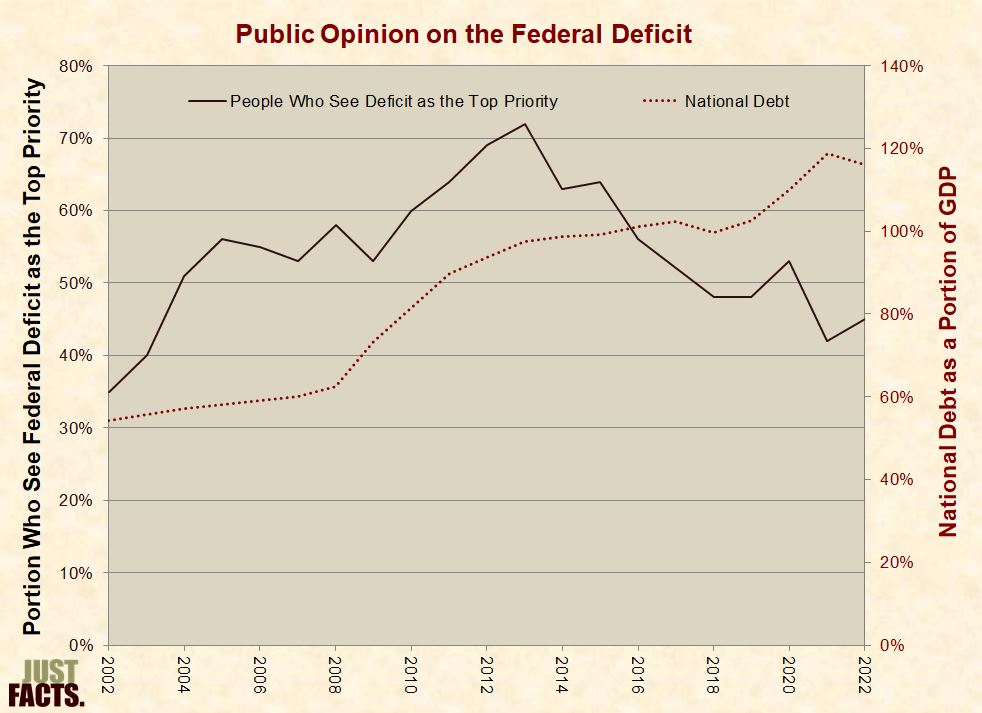

* A series of Pew surveys conducted since 2002 have shown that public concern about the federal deficit has varied with the national debt as follows:

[260] [261] [262] [263] [264] [265]

* A poll conducted by Pew Research Center and USA Today in February 2013 found that:

* A poll conducted by NBC News and the Wall Street Journal in February 2011 found that:

* A poll conducted in November 2010 by the Associated Press and CNBC found that:

* A poll conducted in July 2005 by the Associated Press and Ipsos found that:

* During the first session of the 113th Congress (January–December 2013), U.S. Representatives and Senators introduced 168 bills that would have reduced spending and 828 bills that would have raised spending.[275]

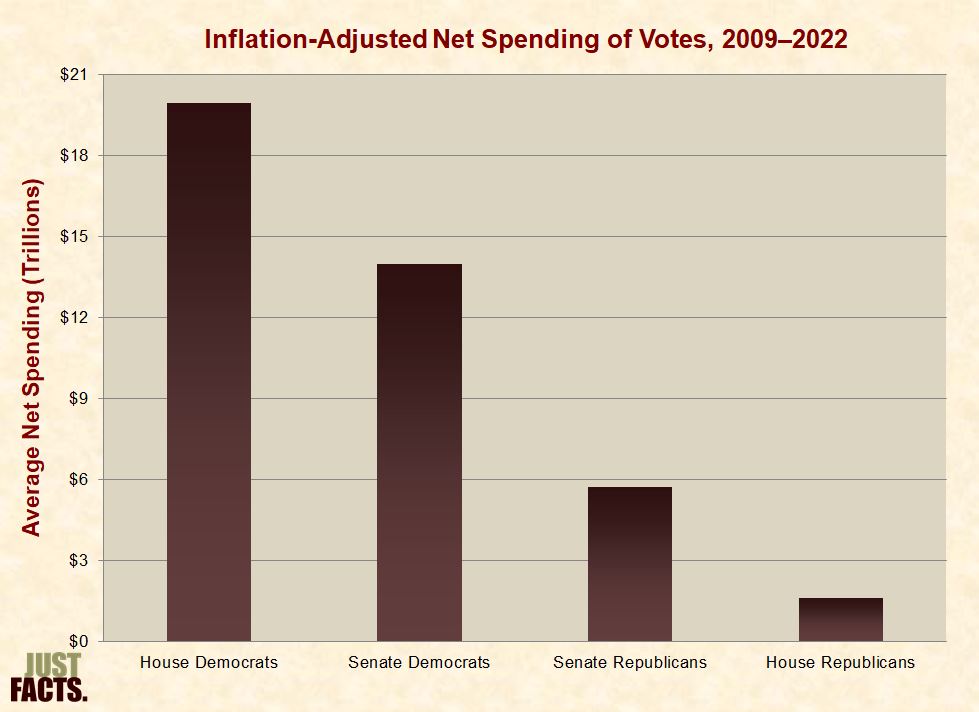

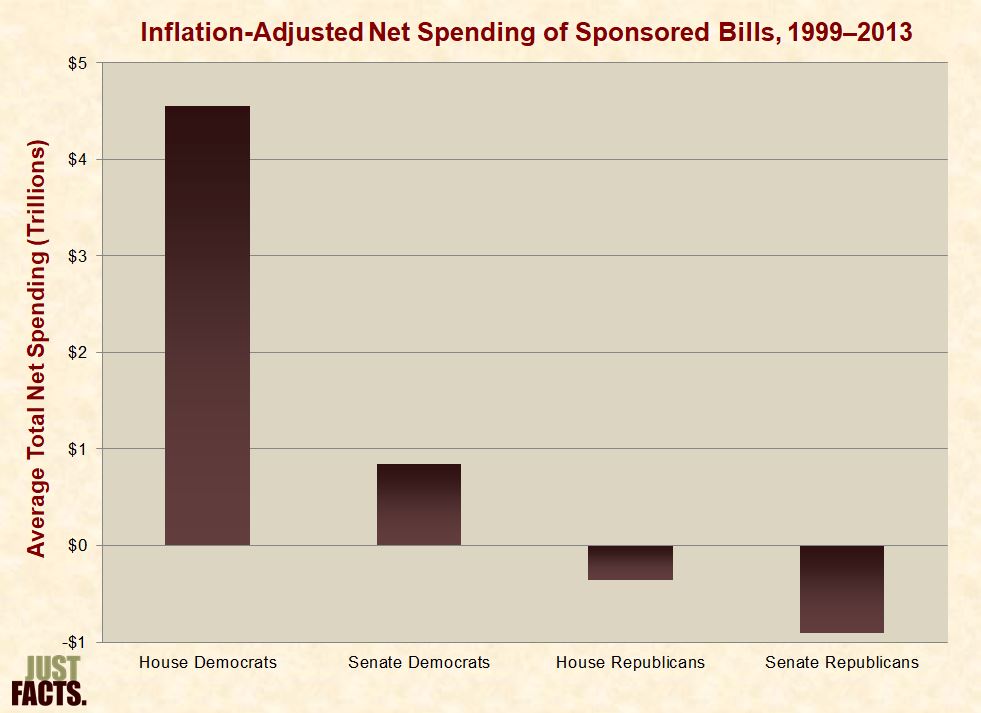

* During the first session of each Congress from 1999 to 2013, the inflation-adjusted increase of net spending in bills sponsored by the average Congressperson from each party totaled:

* In February 2001, Republican President George W. Bush stated:

* From the time that Congress enacted Bush’s first major economic proposal (June 7, 2001[278]) until the time that he left office (January 20, 2009[279]), the national debt rose:

* During eight years in office, Bush vetoed 12 bills, four of which were overridden by Congress and thus enacted without his approval.[284] The Congressional Budget Office projected that these bills would increase the deficit by $26 billion during 2008–2022.[285]

* In February 2009, Democratic President Barack Obama stated:

* From the time that Congress enacted Obama’s first major economic proposal (February 17, 2009[287]) until the time he left office (January 20, 2017[288]), the national debt rose:

* During eight years in office, Obama vetoed 12 bills, one of which was overridden by Congress and thus enacted without his approval.[293] The Congressional Budget Office projected that this bill would “have no significant effect on the federal budget.”[294]

* In March 2016, Republican presidential candidate Donald Trump had the following exchange in an interview with Bob Woodward of the Washington Post:

* From the time that Congress enacted Trump’s first major economic proposal (December 20, 2017[296]) until the outset of the Covid-19 pandemic (March 11, 2020[297]), the national debt rose:

* Before the Covid-19 pandemic, Trump vetoed six bills, none of which were overridden by Congress.[302]

* From the outset of the Covid-19 pandemic (March 11, 2020[303]) until the time Trump left office (January 20, 2021[304]), the national debt rose:

* During the Covid-19 pandemic, Trump vetoed four bills, one of which was overridden by Congress and thus enacted without his approval.[309] The Congressional Budget Office estimated that this bill would increase the deficit by $21 million during 2021–2030.[310]

* State government-imposed lockdowns and other reactions to the Covid-19 pandemic decreased GDP at the end of Trump’s term, thereby increasing the debt/GDP ratio.[311] [312] [313] [314]

* In May 2022, President Biden claimed:

* From the time that Congress enacted Biden’s first major economic proposal (March 10, 2021[316]) until December 31, 2022, the national debt:

* From the beginning of his presidency until December 31, 2022, Biden vetoed one bill, and it was not overridden by Congress.[321]

* The lifting of Covid-19 lockdowns allowed GDP to recover in the first year of Biden’s term, thereby decreasing the debt/GDP ratio.[322] [323] [324] [325]

* As documented in an article published by the Federal Reserve Bank of St. Louis, inflation:

* The finances of some federal programs (like Social Security) are legally separated from the rest of the federal government.[329] When such programs spend less money than they receive, they are legally required to loan any surplus money to the federal government. This adds to the national debt, and the federal government is legally required to pay back these programs with interest.[330] [331] [332] [333] [334] [335]

* The federal government divides the national debt into two main categories:[336] [337]

* Politicians, journalists, and activists often use terms that refer to the total national debt, when in fact they are only referring to a portion of it.[341] To clear up the confusion this has created, below are common terms for the national debt categorized by their correct meanings:

* At the outset of 2023, the $31.4 trillion national debt was comprised of:

* The federal law that governs the repayment of the national debt draws no distinction between publicly held debt and intergovernmental debt. Both must be repaid with interest.[352] [353]

* The White House Office of Management and Budget, the Congressional Budget Office, and other federal agencies sometimes exclude intergovernmental debt in their reckonings of the national debt because this portion of the debt “represents internal transactions of the government and thus has no effect on credit markets.”[354] [355] [356] [357] [358]

* In contrast, federal programs to which this money is owed, such as Social Security and Medicare, include intergovernmental debt and the interest that it generates in their assets and financial projections.[359] [360] [361]

* In the 2000 presidential race, the Gore–Liebermann campaign released a 192-page economic plan that contains over 150 uses of the word “debt.” In none of these instances does the plan mention or account for any intergovernmental debt.[362] The same plan includes intergovernmental debt in the assets of the Social Security and Medicare programs.[363]

* During the federal government’s 2010 fiscal year, the national debt rose from $12.0 trillion to $13.6 trillion, thus increasing by $1.6 trillion.[364] [365]

* The White House, USA Today, Reuters, and other government agencies and media outlets reported that the 2010 federal “deficit” was $1.3 trillion.[366] [367] [368]

* The difference between the national debt increase of $1.6 trillion and the reported deficit of $1.3 trillion is attributable to the following accounting practices:

* PolitiFact, a Pulitzer Prize-winning organization that claims to “help you find the truth in politics,”[372] reported in 2009 that there were “several years of budget surpluses” during Bill Clinton’s presidency. This same article cited the nominal increase in “national debt” during George W. Bush’s presidency.[373] Using the same criterion that PolitiFact applied to Bush’s presidency (the nominal change in national debt since he took office), the national debt rose every year of Clinton’s presidency:

|

Year |

National Debt (Billions) |

|

1993 |

$4,188 |

|

1994 |

$4,501 |

|

1995 |

$4,797 |

|

1996 |

$4,988 |

|

1997 |

$5,310 |

|

1998 |

$5,496 |

|

1999 |

$5,624 |

|

2000 |

$5,706 |

|

2001 |

$5,728 |

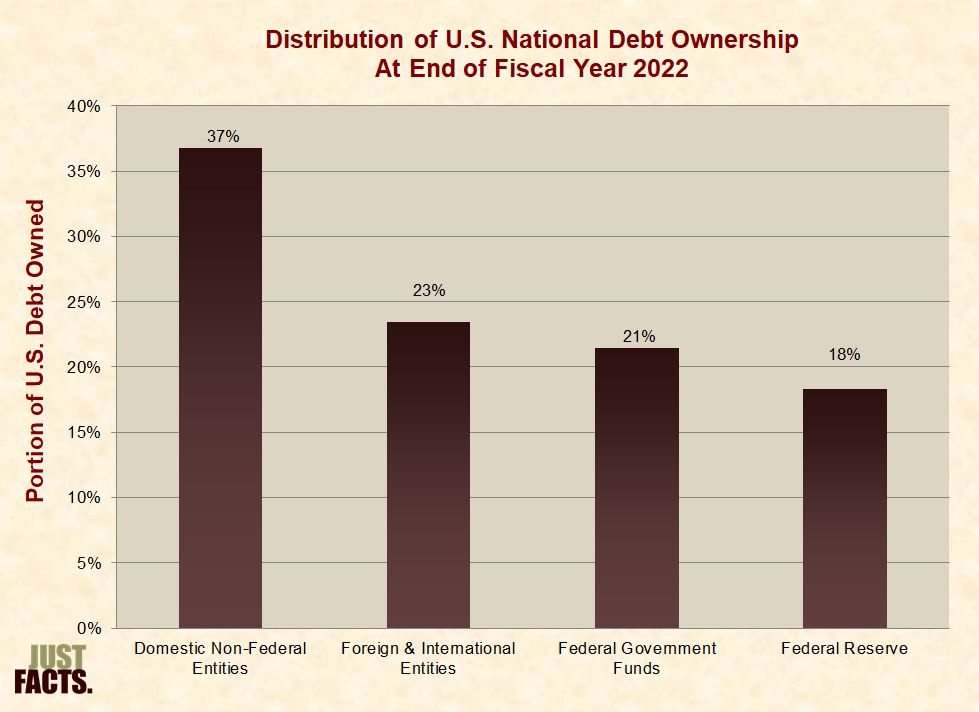

* At the close of the federal government’s 2022 fiscal year on September 30, 2022,[376] the total national debt was $30.9 trillion, and the owners of this debt were:

|

Owner |

Amount (Billions) |

Portion of Total |

|

Domestic Non-Federal Entities |

$11,362 |

37% |

|

Mutual Funds |

$2,606 |

8% |

|

Banks & Savings Institutions |

$1,740 |

6% |

|

State & Local Governments |

$1,537 |

5% |

|

Private Pension Funds |

$750 |

2% |

|

Insurance Companies |

$372 |

1% |

|

State & Local Government Pension Funds |

$366 |

1% |

|

U.S. Savings Bond Holders |

$166 |

1% |

|

Other Investors |

$3,825 |

12% |

|

Foreign & International Entities |

$7,252 |

23% |

|

Japan |

$1,116 |

4% |

|

China |

$902 |

3% |

|

United Kingdom |

$665 |

2% |

|

Belgium |

$325 |

1% |

|

Cayman Islands |

$302 |

1% |

|

Luxembourg |

$300 |

1% |

|

Switzerland |

$273 |

1% |

|

Ireland |

$265 |

1% |

|

Brazil |

$222 |

1% |

|

Taiwan |

$215 |

1% |

|

Other Nations |

$2,666 |

9% |

|

Federal Government Funds |

$6,630 |

21% |

|

Social Security |

$2,838 |

9% |

|

Military Retirement |

$1,195 |

4% |

|

Civil Service Retirement and Disability |

$1,007 |

3% |

|

Medicare |

$345 |

1% |

|

Department of Defense Retiree Healthcare |

$322 |

1% |

|

Deposit Insurance |

$125 |

0.4% |

|

Nuclear Waste Disposal Fund |

$57 |

0.2% |

|

Unemployment Insurance |

$74 |

0.2% |

|

Other Funds |

$667 |

2% |

|

Federal Reserve |

$5,672 |

18% |

|

Total |

$30,915 |

100% |

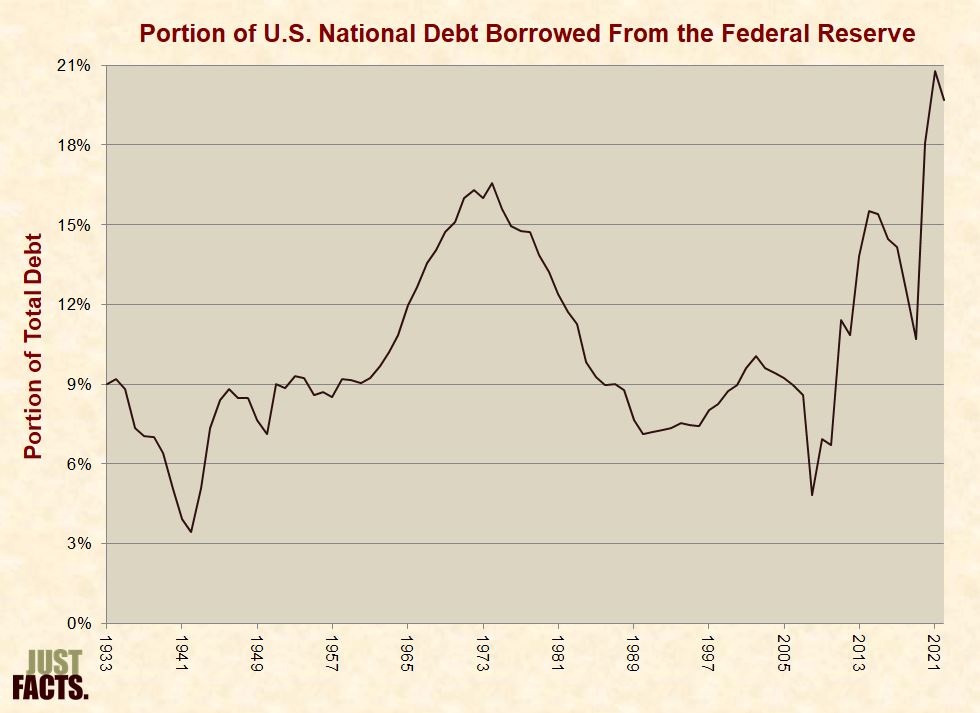

* Since 1933, the portion of the national debt borrowed from the Federal Reserve has varied as follows.

* Recent increases in the amount of debt borrowed from the Federal Reserve are largely due to a policy called quantitative easing.

* At the close of the federal government’s 2022 fiscal year, the $30.9 trillion national debt was comprised of:

|

Amount (Trillions) |

Type |

Portion of Total |

|

$24.3 |

79% |

|

|

$6.6 |

21% |

* At the close of the federal government’s 2022 fiscal year, the publicly held portion of the national debt was $24.3 trillion, and the owners of this debt were:

|

Owner |

Amount (Billions) |

Portion of Publicly Held |

|

Domestic Non-Federal Entities |

$11,362 |

47% |

|

Mutual Funds |

$2,606 |

11% |

|

Banks & Savings Institutions |

$1,740 |

7% |

|

State & Local Governments |

$1,537 |

6% |

|

Private Pension Funds |

$750 |

3% |

|

Insurance Companies |

$372 |

2% |

|

State & Local Government Pension Funds |

$366 |

2% |

|

U.S. Savings Bond Holders |

$166 |

1% |

|

Other Investors |

$3,825 |

16% |

|

Foreign & International Entities |

$7,252 |

30% |

|

Japan |

$1,116 |

5% |

|

China |

$902 |

4% |

|

United Kingdom |

$665 |

3% |

|

Belgium |

$325 |

1% |

|

Cayman Islands |

$302 |

1% |

|

Luxembourg |

$300 |

1% |

|

Switzerland |

$273 |

1% |

|

Ireland |

$265 |

1% |

|

Brazil |

$222 |

1% |

|

Taiwan |

$215 |

1% |

|

Other Nations |

$2,666 |

11% |

|

Federal Reserve[381] |

$5,672 |

23% |

|

Total |

$24,299 |

100% |

* Per the White House Office of Management and Budget, “During most of American history, the Federal debt was held almost entirely by individuals and institutions within the United States,” but foreign and international ownership began to “grow significantly in the early 1970s,” “accelerated” in 1995 to 97, and grew thereafter.[383]

* At the close of the federal government’s 2022 fiscal year, foreign and international entities owned $7.3 trillion of the U.S. national debt, and the owners of this debt were:

|

Owner |

Amount (Billions) |

Portion of Foreign |

|

Japan |

$1,116 |

15% |

|

China |

$902 |

12% |

|

United Kingdom |

$665 |

9% |

|

Belgium |

$325 |

4% |

|

Cayman Islands |

$302 |

4% |

|

Luxembourg |

$300 |

4% |

|

Switzerland |

$273 |

4% |

|

Ireland |

$265 |

4% |

|

Brazil |

$222 |

3% |

|

Taiwan |

$215 |

3% |

|

Other Nations |

$2,666 |

37% |

|

Total |

$7,252 |

100% |

* Foreign purchases of U.S. government debt increase the demand for this debt, thus putting downward pressure on U.S. interest rates. Conversely, foreign sales of U.S. government debt place upward pressure on U.S. interest rates.[385] [386]

* Per a 2008 Congressional Research Service report, a “potentially serious short-term problem would emerge if China decided to suddenly” sell its holding of U.S. government debt. Possible effects could include:

* The same report states:

* During a visit to China in February 2009, Secretary of State Hillary Clinton said:

* In August 2007 during a currency dispute between the U.S. and China, two leading officials of Chinese Communist Party bodies suggested that China use the threat of selling U.S. debt as a “bargaining chip.”[390]

* In February 2009 during a dispute over U.S. arms sales to Taiwan, a Chinese general made the following statements in the state-run magazine Outlook Weekly:

* One month later while appearing before China’s parliament, the head of China’s State Administration of Foreign Exchange said:

* At the close of the federal government’s 2022 fiscal year, the intragovernmental portion of the national debt was $6.6 trillion, and this debt was owned by the following federal trust funds and special funds:

|

Owner |

Amount (Billions) |

Portion of Intragovernmental |

|

Social Security |

$2,838 |

43% |

|

Military Retirement |

$1,195 |

18% |

|

Civil Service Retirement and Disability |

$1,007 |

15% |

|

Medicare |

$345 |

5% |

|

Department of Defense Retiree Healthcare |

$322 |

5% |

|

Deposit Insurance |

$125 |

2% |

|

Nuclear Waste Disposal Fund |

$57 |

1% |

|

Unemployment Insurance |

$74 |

1% |

|

Other Funds |

$667 |

10% |

|

Total |

$6,630 |

100% |

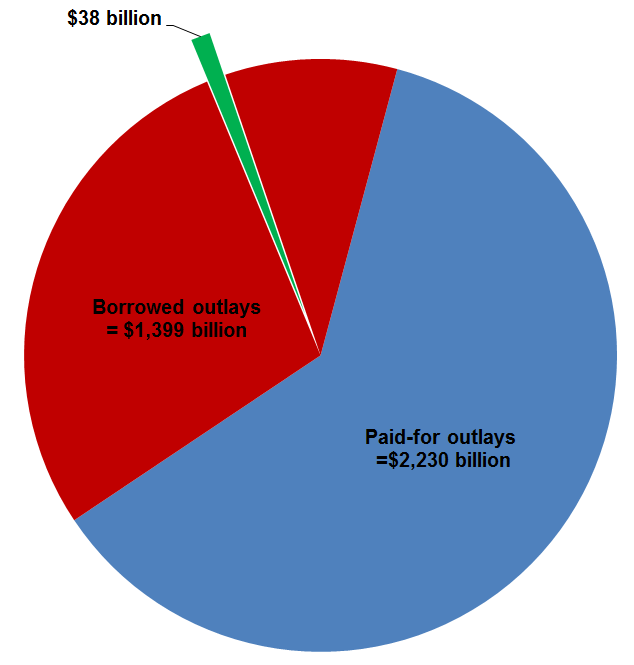

* In April 2011, journalists reported on a $38 billion federal budget cut agreement with the following headlines and verbiage:

* None of the articles above reported that this $38 billion in cuts was primarily from a portion of the budget called “discretionary non-emergency appropriations.”[397] Relative to the entire federal budget, this cut left a projected spending increase of $135 billion from 2010 to 2011. This equates to an inflation-adjusted increase of $49 billion or 0.1 percentage points of the U.S. economy:

* None of the articles above contained a budget-wide frame of reference for the cuts. A spending reduction of $38 billion was 1.0% of the estimated 2011 budget or 2.7% of the deficit:

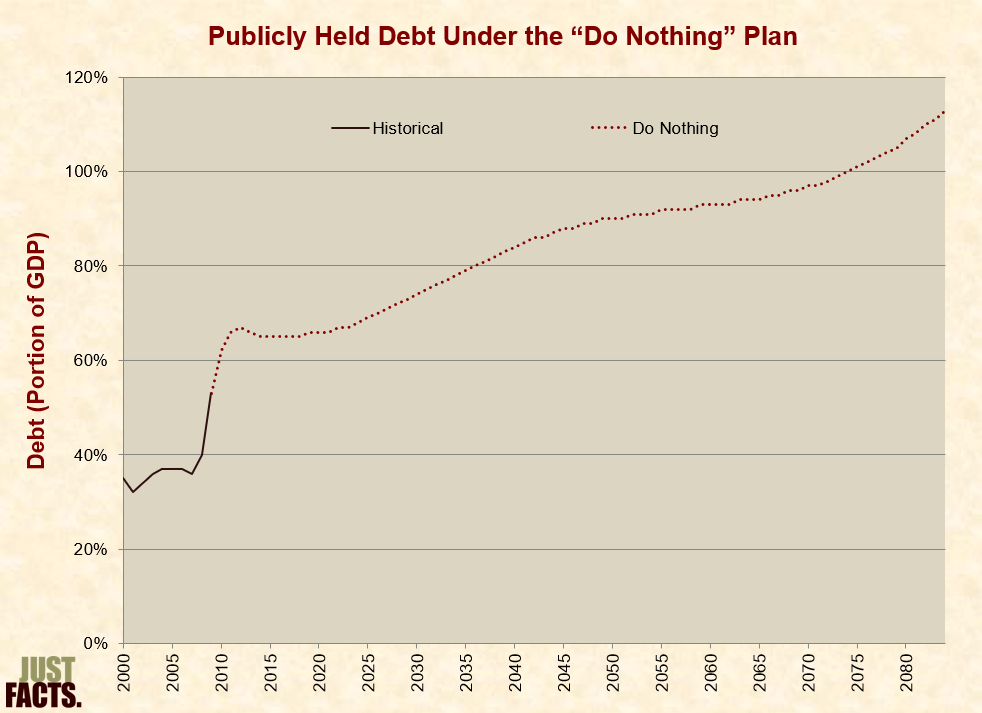

* In a 2011 budget analysis published by the Washington Post, Ezra Klein posted a chart of federal spending and revenue projections based on the Congressional Budget Office’s “current law” scenario and wrote that it:

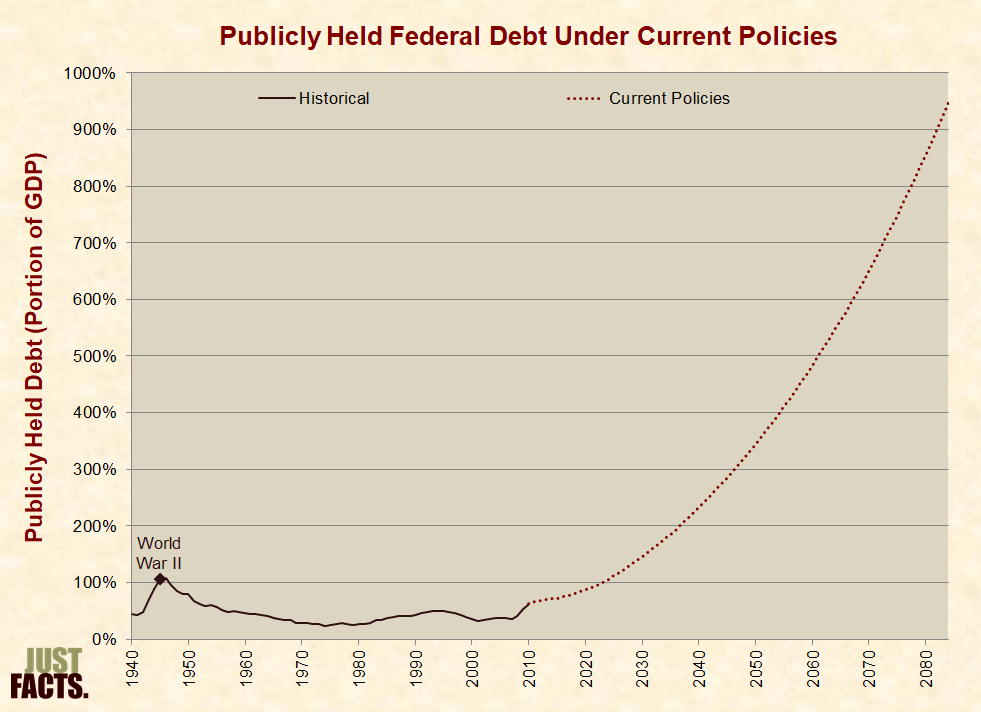

* Klein called this is a “pretty good plan” without revealing that it does not account for interest on the national debt.[402] Under this plan and accounting for this interest, the Congressional Budget Office projected that the publicly held national debt would increase from 62% of the U.S. economy in 2010 to 113% in 2084:

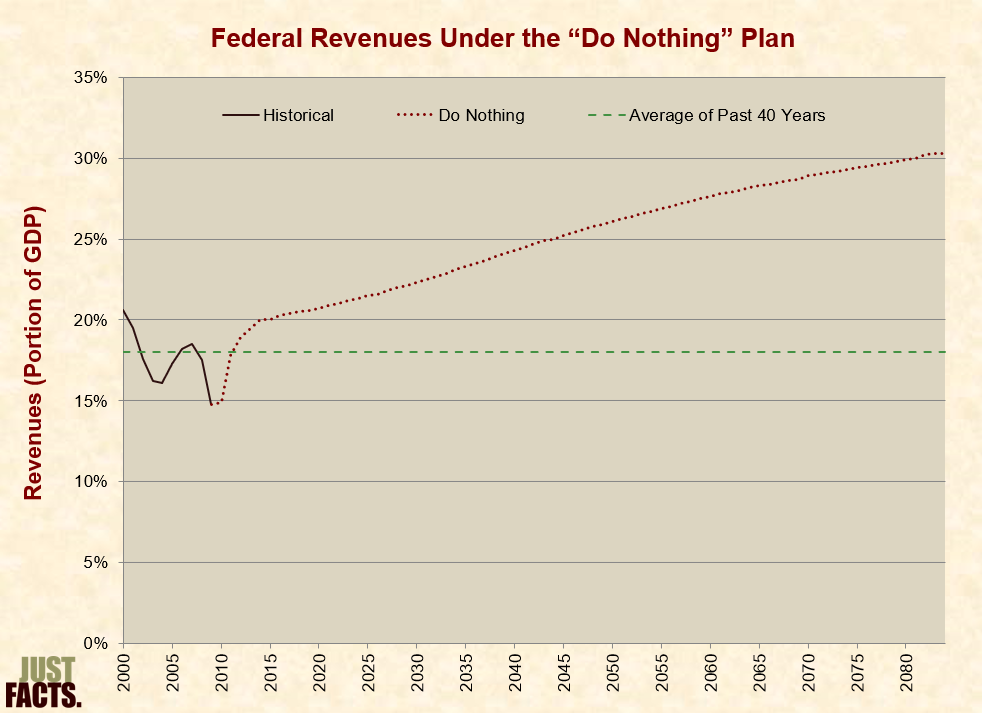

* In the same analysis, Klein claimed that this “do nothing” plan contains “a balanced mix of revenues” and “program cuts” without revealing that under it:[405]

* In February 2010, Fareed Zakaria of CNN stated:

* In 2010, the Bush tax cuts lowered federal revenues by about $283 billion, according to the Congressional Budget Office. This figure of $283 billion:

* President George W. Bush entered office in January of 2001,[415] and he signed tax cuts into law in 2001, 2002, and 2003.[416] [417] In addition to these tax cuts, federal revenues were impacted by factors such as:

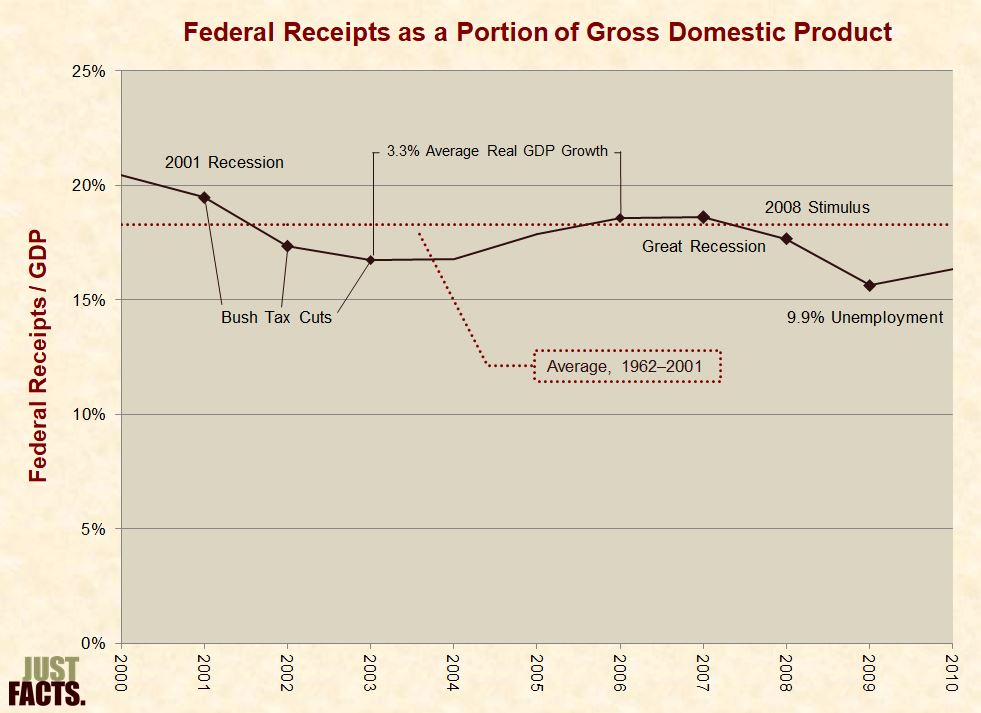

* From 2000 to 2010, federal revenues (as a portion of the U.S. economy or gross domestic product) varied as follows:

* Without mentioning the role of Congress in taxes, spending, or the national debt,[428] [429] PolitiFact reported in 2009 that the national debt increased by $5 trillion “under” George W. Bush, while “there were several years of budget surpluses” at “the end of the Clinton administration.”[430]

* During the tenures of recent presidents and congressional majorities, the average annual changes in national debt (measured in percentage points of GDP) varied as follows:

|

Political Power |

Dates |

Average Annual Debt/GDP Change |

|

Bill Clinton with Democratic House and Senate |

1/20/93–1/4/95 |

0.8 |

|

Bill Clinton with Republican House and Senate |

1/4/95–1/19/01 |

–1.5 |

|

George W. Bush with Republican House and Senate |

1/19/01–6/6/01, 11/12/02–1/4/07 |

0.7 |

|

George W. Bush with Republican House and Democratic Senate |

6/6/01–11/12/02 |

2.2 |

|

George W. Bush with Democratic House and Senate |

1/4/07–1/20/09 |

6.2 |

|

Barack Obama with Democratic House and Senate |

1/20/09–1/5/11 |

9.0 |

|

Barack Obama with Republican House and Democratic Senate |

1/5/11–1/6/15 |

2.3 |

|

Barack Obama with Republican House and Senate |

1/6/15–1/20/17 |

1.7 |

|

Donald Trump with Republican House and Senate |

1/20/17–1/3/19 |

0.1 |

|

Donald Trump with Democratic House and Republican Senate |

1/3/19–1/20/21 |

9.8 |

|

Joseph Biden with Democratic House and Democratic Senate |

1/20/21 – 1/3/23 |

–1.3 |

* Other factors impacting the debt/GDP ratio include but are not limited to high inflation,[432] [433] legislation passed by previous Congresses and presidents,[434] economic cycles, terrorist attacks, pandemics, state government lockdowns, natural disasters, demographics, and the actions of U.S. citizens and foreign governments.[435] [436] [437]

[1] Report: “United States Federal Debt: Answers To Frequently Asked Questions, An Update.” U.S. Government Accountability Office, August 12, 2004. <www.gao.gov>

Page 7:

The amount of any borrower’s debt by itself is not a good indicator of the burden imposed by that debt. A borrower’s income and wealth are important in assessing the burden of debt. Therefore, to get a sense of the burden represented by the federal debt, that debt is often measured in relation to the nation’s income. Gross domestic product (GDP) is a commonly used measure of domestic national income. GDP is the value of all goods and services produced within the United States in a given year and is conceptually equivalent to incomes earned in production. It is a rough indicator of the economic earnings base from which the government draws its revenues. Thus, the ratio of debt held by the public as a share of GDP is a good measure of the burden on the current economy.

[2] Report: “Common Budgetary Terms Explained.” Congressional Budget Office, December 2021. <www.cbo.gov>

“To make comparisons of deficits and federal debt over time, CBO typically measures them as a percentage of gross domestic product (or GDP)—the total market value of all goods and services produced domestically in a given period.”

[3] Article: “Jargon Alert: National Debt.” By David Van Den Berg. Federal Reserve Bank of Richmond Region Focus, Winter 2009. Page 10. <www.richmondfed.org>

“The national debt figures are typically measured as a percentage of gross domestic product (GDP), the primary measure of the nation’s economic activity.”

[4] Report: “Government and Public Sector Debt Measures.” United Kingdom Office for National Statistics, September 2006. <www.ons.gov.uk>

Page 2: “Debt measures are usually presented as a percentage of GDP since comparisons over time need to allow for effects such as inflation. Dividing by GDP is the conventional way of doing this.”

[5] Article: “Government Finance Statistics.” European Union, Eurostat. Accessed May 28, 2020 at <ec.europa.eu>

Introduction

Government finance statistics contain crucial indicators for determining the health of the economies of the EU [European Union] Member States. Under the terms of the EU’s Stability and Growth Pact (SGP), Member States pledged to keep their deficits and debt below certain limits: a Member State’s government deficit may not exceed 3% of its gross domestic product (GDP), while its debt may not exceed 60% of GDP. If a Member State does not respect these limits, the so-called excessive deficit procedure (EDP) is triggered This entails several steps—including the possibility of sanctions—to encourage the Member State concerned to take appropriate measures to rectify the situation. The same deficit and debt limits are also criteria for economic and monetary union (EMU) and hence for joining the euro.

[6] Book: This Time is Different: Eight Centuries of Financial Folly. By Carmen M. Reinhart (University of Maryland) and Kenneth S. Rogoff (Harvard University). Princeton University Press, 2009.

Page 65: “Governments can also default on domestic public debt through high and unanticipated inflation, as the United States and many European countries famously did in the 1970s.”

Page 175:

[I]nflation has long been the weapon of choice in sovereign defaults on domestic debt and, where possible, on international debt. … [G]overnments engage in massive monetary expansion, in part because they can thereby gain a seigniorage tax on real money balances (by inflating down the value of citizens’ currency and issuing more to meet demand). But they also want to reduce, or even wipe out, the real value of public debts outstanding.

Page 400: “Seigniorage is simply the real income a government can realize by exercising its monopoly on printing currency. The revenue can be broken down into the quantity of currency needed to meet the growing transactions demand at constant prices and the remaining growth, which causes inflation, thereby lowering the purchasing power of existing currency.”

[7] Article: “Inflation and the Real Value of Debt: A Double-Edged Sword.” By Christopher J. Neely. Federal Reserve Bank of St. Louis, On the Economy, August 1, 2022. <www.stlouisfed.org>

An increase in the price level directly reduces the real value of government debt, as well as the ratio of debt to GDP [gross domestic product], because—holding other things constant—higher prices increase nominal GDP. Thus, surprise inflation transfers wealth from holders of U.S. government debt—who include both Americans and non-Americans—to U.S. taxpayers.3

This transfer is not an unalloyed good even for U.S. taxpayers, however, because unexpected inflation will tend to raise the cost of servicing future U.S. debt—i.e., nominal yields—by increasing the expected rate of inflation and the risk premium associated with inflation.

[8] Book: Is U.S. Government Debt Different? Edited by Franklin Allen and others. Penn Law, Wharton, FIC Press, 2012. <finance.wharton.upenn.edu>

Chapter 5: “Origins of the Fiscal Constitution.” By Michael W. McConnell (Director of the Constitutional Law Center at Stanford Law School). Pages 45–53.

Pages 49–50:

Section Four of the Amendment states: “The validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned.” This was designed to prevent a southern Democratic majority from repudiating the Civil War debt. … The Supreme Court has interpreted the provision only once, in Perry v. United States2, the so-called Gold Clause Cases. The Court allowed Congress to renege on its contractual agreement to pay the debt in gold; this is when U.S. public debt became denominated in dollars. Effectively, this means that even if Section Four forbids Congress to declare a formal default, it could accomplish much the same thing by inflating the debt away.

[9] Webpage: “Debt to the Penny.” U.S. Department of the Treasury, Bureau of the Fiscal Service. Accessed April 3, 2024 at <fiscaldata.treasury.gov>

“4/1/2024 … Total Public Debt Outstanding [=] $34,627,201,333,064”

[10] Calculated with data from the webpage: “U.S. and World Population Clock.” U.S. Census Bureau, April 3, 2024. <www.census.gov>

“The United States population on April 1, 2024 was: 336,238,570”

CALCULATION: $34,627,201,333,064 debt / 336,238,570 people = $102,984 debt/person

[11] Calculated with the dataset: “Average Number of People per Household, by Race and Hispanic Origin, Marital Status, Age, and Education of Householder: 2023.” U.S. Census Bureau, November 2023. <www2.census.gov>

“Total households [=] 131,434,000”

CALCULATION: $34,627,201,333,064 debt / 131,434,000 households = $261,677 debt/household

[12] Report: “Financial Accounts of the United States: Flow of Funds, Balance Sheets, and Integrated Macroeconomic Accounts, Fourth Quarter 2023.” Board of Governors of the Federal Reserve System, March 7, 2024. <www.federalreserve.gov>

Page 7: “D.3 Debt Outstanding by Sector … Billions of dollars; quarterly figures are seasonally adjusted … Households … Total … 2023Q4 [=] 19,955.2”

CALCULATION: ($34,627,201,333,064 national debt – $19,955,200,000,000 consumer debt) / $19,955,200,000,000 consumer debt = 74%

[13] Calculated with the dataset: “Table 3.2. Federal Government Current Receipts and Expenditures [Billions of Dollars], Seasonally Adjusted at Annual Rates.” U.S. Department of Commerce, Bureau of Economic Analysis. Last revised March 28, 2024. <apps.bea.gov>

|

Total Receipts |

|||

|

2023Q1 |

2023Q2 |

2023Q3 |

2023Q4 |

|

4,651.1 |

4,711.6 |

4,765.4 |

4,864.1 |

CALCULATION: $34,627,201,333,064 debt / (((4,651.1 + 4,711.6 + 4,765.4 + 4,864.1) / 4) × $1,000,000,000 receipts) = 7.3

[14] Calculated with the dataset: “Table 1.1.5. Gross Domestic Product [Billions of Dollars], Seasonally Adjusted at Annual Rates.” U.S. Department of Commerce, Bureau of Economic Analysis. Last revised March 28, 2024. <apps.bea.gov>

|

Gross Domestic Product |

|||

|

2023Q1 |

2023Q2 |

2023Q3 |

2023Q4 |

|

26,813.6 |

27,063.0 |

27,610.1 |

27,957.0 |

CALCULATION: $34,627,201,333,064 debt / (((26,813.6 + 27,063.0 + 27,610.1 + 27,957.0) / 4) × $1,000,000,000 GDP) = 127%

[15] Report: “Budget of the U.S. Government: Fiscal Year 2023.” White House, Office of Management and Budget, March 28, 2022. <www.whitehouse.gov>

Pages 142–143:

Table S–10. Federal Government Financing and Debt (Dollar amounts in billions) …

Debt Outstanding, End of Year …

Total, gross Federal debt … Actual 2021 [=] 28,386 …

As a percent of GDP Actual 2021 [=] 127.0%

[16] Report: “Budget of the U.S. Government: Fiscal Year 2024.” White House, Office of Management and Budget, March 9, 2023. <www.whitehouse.gov>

Pages 168–169:

Table S–10. Federal Government Financing and Debt (Dollar amounts in billions) …

Debt Outstanding, End of Year …

Total, gross Federal debt … Actual 2022 [=] 30,839 …

As a percent of GDP Actual 2022 [=] 123.4%

[17] Blog post: “CBO Releases July 2022 Long-Term Budget Outlook.” Committee for a Responsible Federal Budget, July 27, 2022. <www.crfb.org>

“After rising from 79 percent of Gross Domestic Product (GDP) at the end of Fiscal Year (FY) 2019 to 98 percent of GDP by the end of 2022, CBO projects debt will rise further to 185 percent of GDP by 2052 under current law.”

[18] Commentary: “Spendaholic Politicians Are Destroying Your Economic Future.” By Betsy McCaughey. Creators, January 25, 2023. <www.creators.com>

“The national debt is at the highest level since WWII, and is forecast to break that record soon. In 2022, it hit 98% of GDP—everything we all produce going to work every day—and is growing rapidly.”

[19] Commentary: “Trillions in Debt Reflect a Nation That Has Lost Its Way.” By Star Parker. WND, January 24, 2023. <www.wnd.com>

“How can it be that our national publicly held debt is equal to our entire $25.5 trillion economy? And where were we all when this happened? As recently as 2008, debt was 39.2%, rather than 100%, of our GDP.”

[20] As documented in the three footnotes below from the U.S. Government Accountability Office and the White House Office of Management & Budget:

[21] Report: “United States Federal Debt: Answers To Frequently Asked Questions, An Update.” U.S. Government Accountability Office, August 12, 2004. <www.gao.gov>

Page 1: “Debt held by the public plus debt held by government accounts represent total debt, or gross federal debt.”

Pages 10–11:

Debt held by the public approximates current federal demand on credit markets. It represents a burden on today’s economy, and the interest paid on this debt represents a burden on current taxpayers. …

However, debt held by government accounts reflects a future burden on taxpayers and the economy. The special federal securities held in the accounts represent legal obligations of the Treasury and are guaranteed for principal and interest by the full faith and credit of the U.S. government.

[22] Report: “Budget of the U.S. Government: Fiscal Year 2023.” White House, Office of Management and Budget, March 28, 2022. <www.whitehouse.gov>

Pages 142–143:

Table S–10. Federal Government Financing and Debt (Dollar amounts in billions) …

Debt Outstanding, End of Year …

Total, gross Federal debt … Actual 2021 [=] 28,386 …

As a percent of GDP Actual 2021 [=] 127.0% …

Debt held by Government accounts … Actual 2021 [=] 6,102 …

Debt held by the public … Actual 2021 [=] 22,284 …

As a percent of GDP Actual 2021 [=] 99.7%

[23] Report: “Budget of the U.S. Government: Fiscal Year 2024.” White House, Office of Management and Budget, March 9, 2023. <www.whitehouse.gov>

Pages 168–169:

Table S–10. Federal Government Financing and Debt (Dollar amounts in billions) …

Debt Outstanding, End of Year …

Total, gross Federal debt … Actual 2022 [=] 30,839 …

As a percent of GDP Actual 2022 [=] 123.4% …

Debt held by Government accounts … Actual 2022 [=] 6,586 …

Debt held by the public … Actual 2022 [=] 24,252 …

As a percent of GDP Actual 2022 [=] 97%

[24] Calculated with data from:

a) Dataset: “Historical Debt Outstanding—Annual, 1790–1849.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

b) Dataset: “Historical Debt Outstanding—Annual, 1850–1899.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

c) Dataset: “Historical Debt Outstanding—Annual, 1900–1949.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

d) Dataset: “Historical Debt Outstanding—Annual, 1950–1999.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

e) Webpage: “Debt to the Penny.” U.S. Department of the Treasury, Bureau of the Fiscal Service. Accessed March 3, 2023 at <fiscaldata.treasury.gov>

f) Dataset: “Historical Data on the Federal Debt.” Congressional Budget Office, August 5, 2010. <www.cbo.gov>

g) Dataset: “Table 1.1.5. Gross Domestic Product [Billions of Dollars].” United States Department of Commerce, Bureau of Economic Analysis. Last revised February 28, 2024. <apps.bea.gov>

NOTE: An Excel file containing the data and calculations is available upon request.

[25] “WHO Director-General’s Opening Remarks at the Media Briefing on Covid-19.” World Health Organization, March 11, 2020. <bit.ly>

[Dr. Tedros Adhanom Ghebreyesus:] …

WHO has been assessing this outbreak around the clock and we are deeply concerned both by the alarming levels of spread and severity, and by the alarming levels of inaction.

We have therefore made the assessment that COVID-19 can be characterized as a pandemic.

[26] Calculated with data from:

a) Dataset: “Historical Debt Outstanding—Annual, 1790–1849.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

b) Dataset: “Historical Debt Outstanding—Annual, 1850–1899.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

c) Dataset: “Historical Debt Outstanding—Annual, 1900–1949.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

d) Dataset: “Historical Debt Outstanding—Annual, 1950–1999.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

e) Webpage: “Debt to the Penny.” U.S. Department of the Treasury, Bureau of the Fiscal Service. Accessed March 2, 2023 at <fiscaldata.treasury.gov>

f) Dataset: “Historical Data on the Federal Debt.” Congressional Budget Office, August 5, 2010. <www.cbo.gov>

g) Dataset: “Table 1.1.5. Gross Domestic Product [Billions of Dollars].” United States Department of Commerce, Bureau of Economic Analysis. Last revised February 28, 2024. <apps.bea.gov>

NOTES: An Excel file containing the data and calculations is available upon request.

[27] Article: “World War II.” Encyclopædia Britannica Ultimate Reference Suite 2004.

[It was] also called Second World War, a conflict that involved virtually every part of the world during the years 1939–45. The principal belligerents were the Axis powers—Germany, Italy, and Japan—and the Allies—France, Great Britain, the United States, the Soviet Union, and, to a lesser extent, China. The war was in many respects a continuation, after an uneasy 20-year hiatus, of the disputes left unsettled by World War I. The 40,000,000–50,000,000 deaths incurred in World War II make it the bloodiest conflict as well as the largest war in history.

[28] Calculated with data from:

a) Dataset: “Historical Debt Outstanding—Annual, 1790–1849.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

b) Dataset: “Historical Debt Outstanding—Annual, 1850–1899.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

c) Dataset: “Historical Debt Outstanding—Annual, 1900–1949.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

d) Dataset: “Historical Debt Outstanding—Annual, 1950–1999.” United States Department of the Treasury, Bureau of the Public Debt. Updated May 5, 2013. <www.justfacts.com>

e) Webpage: “Debt to the Penny.” U.S. Department of the Treasury, Bureau of the Fiscal Service. Accessed March 2, 2023 at <fiscaldata.treasury.gov>

f) Dataset: “Historical Data on the Federal Debt.” Congressional Budget Office, August 5, 2010. <www.cbo.gov>

g) Dataset: “Table 1.1.5. Gross Domestic Product [Billions of Dollars].” United States Department of Commerce, Bureau of Economic Analysis. Last revised January 26, 2023. <apps.bea.gov>

NOTE: An Excel file containing the data and calculations is available upon request.

[29] Webpage: “About GAO.” U.S. Government Accountability Office. Accessed July 2, 2020 at <www.gao.gov>

The U.S. Government Accountability Office (GAO) is an independent, nonpartisan agency that works for Congress. Often called the “congressional watchdog,” GAO examines how taxpayer dollars are spent and provides Congress and federal agencies with objective, reliable information to help the government save money and work more efficiently.

[30] Report: “United States Federal Debt: Answers To Frequently Asked Questions, An Update.” U.S. Government Accountability Office, August 12, 2004. <www.gao.gov>

Pages 65–67:

Debt held by the public is the largest explicit liability of the federal government. However, the federal government undertakes a wide range of programs, responsibilities, and activities that may explicitly or implicitly expose it to future spending. These “fiscal exposures”2 vary widely as to source, extent of the government’s legal obligation, likelihood of occurrence, and magnitude. Given this variety, it is useful to think of fiscal exposures as a spectrum extending from explicit liabilities to the implicit promises embedded in current policy or public expectations. (See table 2.) For example, the current liability figures for the U.S. government do not include the difference between scheduled and funded benefits in connection with the Social Security and Medicare programs.

Fiscal exposures represent significant commitments that ultimately have to be addressed. The burden of paying for these exposures may encumber future budgets and constrain fiscal flexibility. Not capturing the long-term costs of current decisions limits policymakers’ ability to control the government’s fiscal exposures at the time decisions are made. In addition, the lack of recognition of long-term fiscal exposures may make it difficult for policymakers and the public to adequately understand the government’s overall performance and true financial condition.

[31] Report: “Federal Insurance and Other Activities that Transfer Risk or Losses to the Government.” U.S. Government Accountability Office, March 2019. <www.gao.gov>

Page 2 (of PDF):

Through analysis of sources containing government-wide information on federal activities, GAO [U.S. Government Accountability Office] identified 148 federal insurance and other activities that transfer risk or losses from adverse events to the government…. Unlike private insurance, the activities do not necessarily have a contract or charge premiums or fees in exchange for assuming risk. Even when premiums or fees exist they may not cover all costs, as federal expenditures can be driven by policy goals or agency missions rather than the aim of fiscal solvency. …

The government’s primarily cash-based budget generally does not record the full cost of commitments incurred until corresponding payments are made in the future. Therefore, the budget may not accurately reflect federal costs or the likely claim on federal resources for such activities. For some claims, such as pension and life insurance, the federal commitment occurs years before payments are reflected in the budget. Additionally, payments the government may be expected to make based on policies or past practices (but is not legally required to make) may not be evident in the budget. … GAO previously recommended … that Congress consider expanding the use of accrual-based information in the budget documents submitted to Congress. However, this recommendation has not been implemented. Accrual measurement would provide enhanced control over future spending by recognizing long-term costs when decisions are made.

Page 39:

The government undertakes a wide range of activities that create fiscal exposures by obligating the government to future spending or creating an expectation for such spending. The federal budget both allocates and controls resources, but does not provide complete information about some significant fiscal exposures. Failure to understand and address these exposures can have significant consequences. These fiscal exposures will require future federal spending and will absorb resources available for other activities. Not capturing the long-term costs of current decisions limits Congress’s ability to control federal fiscal exposures at the time decisions are made. Presenting accrual information alongside cash-based budget numbers, particularly in areas where it would enhance up-front control of budgetary resources, would be useful to policymakers when debating current activities and considering new legislation.

[32] Report: “Enron: Selected Securities, Accounting, and Pension Laws Possibly Implicated in its Collapse.” By Michael V. Seitzinger, Marie B. Morris, and Mark Jickling. Congressional Research Service, Library of Congress, January 16, 2002. <www.justfacts.com>

Page 2:

Among the disclosures of publicly traded companies are accounting statements. Since financial information is of little use to investors unless all firms use comparable accounting methods, the securities laws give the Securities and Exchange Commission broad authority to establish standards for financial reporting. The SEC [U.S. Securities and Exchange Commission] has delegated the task of writing accounting standards to private sector bodies, and since 1973 the Financial Accounting Standards Board has been charged with formulating accounting and financial reporting standards.

[33] Summary of Statement No. 106: “Employers’ Accounting for Postretirement Benefits Other Than Pensions.” Financial Accounting Standards Board, December 1990. <bit.ly>

This Statement establishes accounting standards for employers’ accounting for postretirement benefits other than pensions…. It will significantly change the prevalent current practice of accounting for postretirement benefits on a pay-as-you-go (cash) basis by requiring accrual, during the years that the employee renders the necessary service, of the expected cost of providing those benefits to an employee and the employee’s beneficiaries and covered dependents. …

… The Board believes that measurement of the obligation and accrual of the cost based on best estimates are superior to implying, by a failure to accrue, that no obligation exists prior to the payment of benefits. The Board believes that failure to recognize an obligation prior to its payment impairs the usefulness and integrity of the employer’s financial statements. …

The provisions of this Statement are similar, in many respects, to those in FASB [Financial Accounting Standards Board] Statements No. 87, Employers’ Accounting for Pensions, and No. 88, Employers’ Accounting for Settlements and Curtailments of Defined Benefit Pension Plans and for Termination Benefits. …

This Statement relies on a basic premise of generally accepted accounting principles that accrual accounting provides more relevant and useful information than does cash basis accounting. …

[L]ike accounting for other deferred compensation agreements, accounting for postretirement benefits should reflect the explicit or implicit contract between the employer and its employees.

[34] Book: Finance for Managers. By Richard Luecke and Samuel L. Hayes. Harvard Business School Press, 2002.

Page 39:

In contrast to cash-basis accounting, accrual accounting records transactions as they are made, whether or not the cash has actually changed hands. Most companies of any size use accrual accounting. This system provides a better matching between revenues and their associated cost, which helps companies understand the true causes and effect of business activities. Accordingly, revenues are recognized during the period in which the sales activities occur, whereas expenses are recognized in the same period as their associated revenues.

[35] Report: “Understanding the Primary Components of the Annual Financial Report of the United States Government.” U.S. Government Accountability Office, September, 2005. <www.gao.gov>

Page 5:

Accrual accounting, which is also used by private business enterprises, is the basis for U.S. generally accepted accounting principles for federal government entities. It is intended to provide a complete picture of the federal government’s financial operations and financial position. The federal government primarily uses the cash basis of accounting for its budget, which is the federal government’s primary financial planning and control tool.

Page 6:

The accrual basis of accounting recognizes revenue when it is earned and recognizes expenses in the period incurred, without regard to when cash is received or disbursed. The federal government, which receives most of its revenue from taxes, nevertheless recognizes tax revenue when it is collected, under an accepted modified cash basis of accounting.

[36] Calculated with data from: “Fiscal Year 2022 Financial Report of the United States Government.” U.S. Department of the Treasury, February 16, 2023. <fiscal.treasury.gov>

Page 65:

United States Government Balance Sheets as of September 30, 2022, and 2021

|

Liabilities |

2022 (billions $) |

|

Accounts payable |

114.6 |

|

Federal employee and veteran benefits payable |

12,811.9 |

|

Environmental and disposal liabilities |

626.3 |

|

Benefits due and payable |

288.3 |

|

Loan guarantee liabilities |

6.4 |

|

Insurance and guarantee program liabilities |

104.5 |

|

Advances from others and deferred revenues |

247.2 |

|

Other liabilities |

495.1 |

|

Total of above (excludes publicly held federal debt) |

14,694 |

[37] The following points provide important context for understanding the data and calculation in the next footnote:

[38] Calculated with data from the “2022 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” United States Social Security Administration, June 7, 2022. <www.ssa.gov>

Page 7: “Table II.B1.—Summary of 2021 Trust Fund Financial Operations [In billions]. … OASDI [Social Security] … Asset reserves at the end of 2021 … $2,852.0”

Page 209:

Table VI.F2.—Present Values Through the Infinite Horizon for Various Categories of Program Participants, Based on Intermediate Assumptions [Present values as of January 1, 2022; dollar amounts in trillions] …

present value of future cost for current participants [=] $91.0 …

present value of future dedicated tax income for current participants [=] $42.4 …

present value of future General Fund reimbursements through the infinite horizon a [=] d …

a Distribution of General Fund reimbursements among past, current, and future participants cannot be determined.

d Less than $50 billion

CALCULATION:

$91.0 trillion present value of future cost for current participants

– $42.4 trillion present value of future dedicated tax income for current participants

– $0.05 trillion present value of future general fund reimbursements over the infinite horizon

– $2.852 trillion current value of the trust fund

= $45.698 trillion closed group unfunded obligation

[39] A very common but false belief is that the Social Security program has been looted. For facts about this myth, visit Just Facts’ research on Social Security.

[40] The following points provide important context for understanding the data and calculation in the next footnote:

[41] Calculated with data from the “2022 Annual Report of the Board of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds.” United States Department of Health and Human Services, Centers for Medicare and Medicaid Services, June 2, 2022. <www.cms.gov>

Page 12: “Table II.B1.—Medicare Data for Calendar Year 2021 … Assets at end of 2020 (billions) … Total [=] $277.4”

Page 212:

The first line of table V.G2 [which displays unfunded Part A obligations] shows the present value of future expenditures less future taxes for current participants, including both beneficiaries and covered workers [i.e., taxpayers]. Subtracting the current value of the HI [Hospital Insurance or Part A] trust fund (the accumulated value of past HI taxes less outlays) results in a closed-group unfunded obligation of $14.5 trillion.

Page 215: “Table V.G4.—Unfunded Part B Obligations for Current and Future Program Participants through the Infinite Horizon [Present values as of January 1, 2022; dollar amounts in trillions] … Equals unfunded obligations for past and current participants1 … General revenue contributions [=] $32.2”

Page 217: “Table V.G6.—Unfunded Part D Obligations for Current and Future Program Participants through the Infinite Horizon [Present values as of January 1, 2022; dollar amounts in trillions] … Equals unfunded obligations for past and current participants1 … General revenue contributions [=] $5.9”

CALCULATION: $14.5 trillion in closed-group unfunded obligations for Medicare Part A + $32.2 trillion in closed-group unfunded obligations for Part B + $5.9 trillion in closed-group unfunded obligations for Part D = $52.6 trillion in closed-group unfunded obligations for the Medicare program

[42] See here, here, and here for documentation that publicly traded companies are required by law to calculate their debt and obligations using accrual accounting. The next three footnotes document that:

The Treasury’s annual Financial Report of the United States Government was originally the source for all of the above-cited federal liabilities and obligations. However, in 2009, the Treasury stopped publishing individual closed-group obligations for Social Security and Medicare. Since then, the report has only shown the combined total of closed-group obligations for all social insurance programs. For the 2009 and 2010 reports, Just Facts requested and received the components of this total from the Treasury. For the 2011 report, the Treasury did not provide these figures despite repeated requests. Thus, Just Facts now calculates these figures using data from the Social Security and Medicare Trustees Reports. This methodology is detailed in the four footnotes above and produces results that are consistent with the individual data released by the Treasury in earlier reports.

[43] Pages 16–17:

Each year, the Administration issues two reports that detail the government’s financial results: the [federal] Budget and this Financial Report. The exhibit on the following page provides the key characteristics and differences between the two documents.

Treasury generally prepares the financial statements in this Financial Report on an accrual basis of accounting as prescribed by GAAP [Generally Accepted Accounting Principles] for federal entities. …

Budget of the U.S. Government: Prepared primarily on a “cash basis” …

Financial Report of the U.S. Government: Prepared on an “accrual basis” and “modified cash basis”

[44] Report: “Federal Insurance and Other Activities that Transfer Risk or Losses to the Government.” U.S. Government Accountability Office, March 2019. <www.gao.gov>

Page 2 (of PDF):

The government’s primarily cash-based budget generally does not record the full cost of commitments incurred until corresponding payments are made in the future. Therefore, the budget may not accurately reflect federal costs or the likely claim on federal resources for such activities. For some claims, such as pension and life insurance, the federal commitment occurs years before payments are reflected in the budget. Additionally, payments the government may be expected to make based on policies or past practices (but is not legally required to make) may not be evident in the budget. … GAO [U.S. Government Accountability Office] previously recommended … that Congress consider expanding the use of accrual-based information in the budget documents submitted to Congress. However, this recommendation has not been implemented. Accrual measurement would provide enhanced control over future spending by recognizing long-term costs when decisions are made.

Page 39:

The government undertakes a wide range of activities that create fiscal exposures by obligating the government to future spending or creating an expectation for such spending. The federal budget both allocates and controls resources, but does not provide complete information about some significant fiscal exposures. Failure to understand and address these exposures can have significant consequences. These fiscal exposures will require future federal spending and will absorb resources available for other activities. Not capturing the long-term costs of current decisions limits Congress’s ability to control federal fiscal exposures at the time decisions are made. Presenting accrual information alongside cash-based budget numbers, particularly in areas where it would enhance up-front control of budgetary resources, would be useful to policymakers when debating current activities and considering new legislation.

[45] Report: “Understanding the Primary Components of the Annual Financial Report of the United States Government.” U.S. Government Accountability Office, September, 2005. <www.gao.gov>

Page 5:

Accrual accounting, which is also used by private business enterprises, is the basis for U.S. generally accepted accounting principles for federal government entities. It is intended to provide a complete picture of the federal government’s financial operations and financial position. The federal government primarily uses the cash basis of accounting for its budget, which is the federal government’s primary financial planning and control tool.

Page 6:

The accrual basis of accounting recognizes revenue when it is earned and recognizes expenses in the period incurred, without regard to when cash is received or disbursed. The federal government, which receives most of its revenue from taxes, nevertheless recognizes tax revenue when it is collected, under an accepted modified cash basis of accounting.

[46] Textbook: Fiscal Challenges: An Interdisciplinary Approach to Budget Policy. Edited by Elizabeth Garrett, Elizabeth A. Graddy, and Howell E. Jackson. Cambridge University Press, 2009.

Chapter 6: “Counting the Ways: The Structure of Federal Spending.” By Howell E. Jackson.

Page 207: “The measure featured here is the ‘closed-group liability’ for each program. This measure reflects the financial burden or liability being passed on to future generations.”

[47] “2010 Annual Report of the Board of Trustees of The Federal Old-Age and Survivors Insurance and Disability Insurance Trust Funds.” Board of Trustees of the Federal OASDI Trust Funds, August 9, 2010. <www.ssa.gov>

Page 65: “[The] closed group unfunded obligation … represents the shortfall of lifetime contributions for all past† and current participants relative to the cost of benefits for them.”

Page 209 [appendix]: “Closed group unfunded obligation. This measure is computed like the open group unfunded obligation except that individuals under the age of 15 (or not yet born) are excluded. In other words, only persons who attain age 15 or older during the first year of the projection period are included in the calculations.”

NOTES:

[48] “2009 Financial Report of the United States Government.” U.S. Department of the Treasury, 2009. <www.fiscal.treasury.gov>

Page 43:

The [social insurance] estimates are actuarial present values2 of the projections and are based on the economic and demographic assumptions representing the trustees’ best estimates as set forth in the relevant Social Security and Medicare trustees’ reports and in the relevant agency performance and accountability reports for the RRB [Railroad Retirement Board] and the DOL [Department of Labor] (Black Lung). …

2 Present values recognize that a dollar paid or collected in the future is worth less than a dollar today, because a dollar today could be invested and earn interest. To calculate a present value, future amounts are thus reduced using an assumed interest rate, and those reduced amounts are summed.

Page 52:

Participants for the Social Security and Medicare programs are assumed to be the “closed group” of individuals who are at least age 15 at the start of the projection period, and are participating as either taxpayers, beneficiaries, or both, except for the 2007 Medicare programs for which current participants are assumed to be at least 18 instead of 15 years of age.

Page 125:

Current participants in the Social Security and Medicare programs form the “closed group” of taxpayers and/or beneficiaries who are at least age 15 at the start of the projection period. For the 2007 Medicare projections, current participants are at least 18 years of age at the beginning of the projection period. Since the projection period for the Social Security, Medicare, and Railroad Retirement social insurance programs consists of 75 years, the period covers virtually all of the current participants’ working and retirement years, a period that could be greater than 75 years in a relatively small number of instances.

[49] Report: “Social Security and Medicare Trust Funds and the Federal Budget.” U.S. Department of Treasury, Office of Economic Policy, May 2009. <www.treasury.gov>

Page 16: “The resulting present value is the amount that would have to be put in the bank today at the assumed interest rate to fund the future cash flows.”

[50] “Fiscal Year 2022 Financial Report of the United States Government.” U.S. Department of the Treasury, February 16, 2023. <fiscal.treasury.gov>

Pages 5–6:

More than three-fourths of the federal government’s total assets ($5.0 trillion) consist of: 1) $877.8 billion in cash and monetary assets; 2) $406.9 billion in inventory and related property; 3) $1.4 trillion in net loans receivable (primarily student loans); and 4) $1.2 trillion in net PP&E. …

Other significant government resources not reported on the Balance Sheet include the government’s power to tax and set monetary policy, natural resources, and stewardship assets.

Page 162:

Stewardship PP&E [property, plant, and equipment] consists of items whose physical properties resemble those of general PP&E traditionally capitalized in financial statements. However, stewardship PP&E differs from general PP&E in that their values may be indeterminable or may have little meaning (e.g., museum collections, monuments, assets acquired in the formation of the nation) or that allocating the cost of such assets to accounting periods that benefit from the ownership of such assets is meaningless. Stewardship PP&E includes stewardship land (land not acquired for or in connection with general PP&E) and heritage assets (e.g., federal monuments and memorials and historically or culturally significant property).

Stewardship land is land and land rights owned by the federal government intended to be held indefinitely. The majority of stewardship land was acquired by the government during the first century of the nation’s existence. Examples of stewardship land include land reserved, managed, planned, used, or acquired for forests and parks, recreation and conservation, wildlife and grazing, historical landmarks, multiple purpose ancillary revenue generating activities, and/or buffer zones. “Land” is defined as the solid part of the surface of the earth. Excluded from the definition are the natural resources (that is, depletable resources, such as mineral deposits and petroleum; renewable resources, such as timber; and the outer-continental shelf resources) related to land. …

Heritage assets are government-owned assets that have one or more of the following characteristics: historical or natural significance; cultural, educational, or artistic importance; or significant architectural characteristics. Entities provide protection and preservation services to maintain all heritage assets in the best possible condition as part of America’s history. Examples of heritage assets include the Declaration of Independence, the U.S. Constitution, and the Bill of Rights preserved by the National Archives. Heritage assets are classified into two categories: collection and non-collection. Collection type heritage assets include objects gathered and maintained for exhibition, for example, museum collections, art collections, and library collections. Non-collection type heritage assets include parks, memorials, monuments, and buildings. In some cases, heritage assets may serve two purposes: a heritage function and general government operations. In those cases, the heritage asset should be considered a multi-use heritage asset if the predominant use of the asset is in general government operations (e.g., the main Treasury building used as an office building). The cost of acquisition, improvement, reconstruction, or renovation of multi-use heritage assets should be capitalized as general PP&E and depreciated over its estimated useful life.